Dean Baker nails it. The very existence of this sort of trading apparatus, which benefits only the company deploying it, relies entirely on what

should be privileged knowledge (e.g. foreknowledge of trade patterns about to happen that can only be extracted and acted upon through either initiating the trade itself or privileged placement of what amounts to a compute cluster on a particular routing switch (or both)), and is the sort of thing used by Goldman

et al. to, you know,

screw their own customers by trading against their interests and/or simply profiting off what amounts to insider information, is as anti-market, anti-competitive, and the very essence of what all our anti-collusion, anti-insider trading, anti-trust, and anti-monopoly laws are intended to control.

And these types of transactions

do nothing for the broader economy beyond radically enriching a handful of folks who can

only spend so much. And we’re a country with a

giant aggregate demand problem. So there’s that.

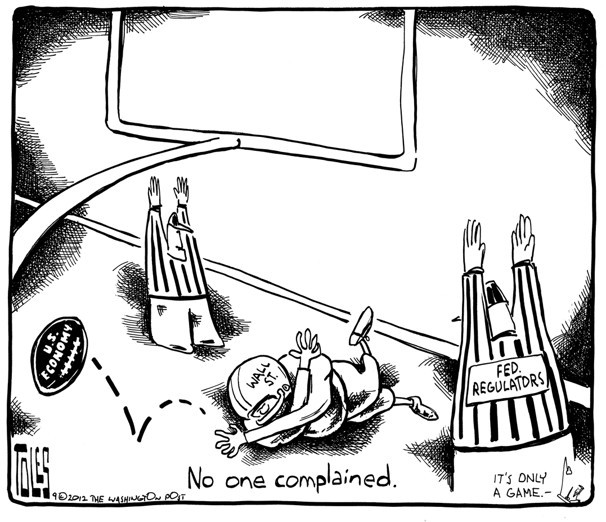

But may the Flying Spaghetti Monster help anyone who tries to regulate this practice

in any way, much less apply a nominal cost to such actions. This, along with rampant and abusive

naked shorting, is the true scandal of Wall Street. (By the by: naked shorting is already illegal, but is basically never even

investigated, much less litigated. In light of recent events, this should be the basis of a scandal…but that would require a functioning media. Look over there! A missing white woman!)

And, so far as I can tell, exactly zero is being done about any of it. And nothing will be done until after the

next financial collapse. And it will only happen

then if the collapse is sufficiently devastating that the entire structure of Wall Street finance is utterly laid waste (thus ending their political influence in the aftermath). Sounds like a time.